Happy Wednesday and welcome back to On The Money, now 0.25 percentage points cheaper. I’m Sylvan Lane, and here’s your nightly guide to everything affecting your bills, bank account and bottom line.

See something I missed? Let me know at slane@digital-stage.thehill.com or tweet me @SylvanLane. And if you like your newsletter, you can subscribe to it here: http://bit.ly/1NxxW2N.

Write us with tips, suggestions and news: slane@digital-stage.thehill.com, njagoda@digital-stage.thehill.com and nelis@digital-stage.thehill.com. Follow us on Twitter: @SylvanLane, @NJagoda and @NivElis.

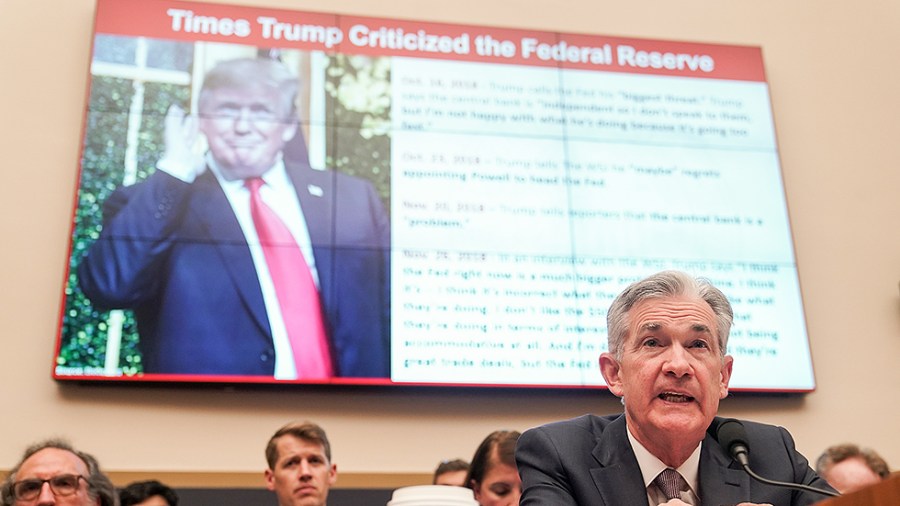

THE BIG DEAL– Fed cuts interest rates for first time since financial crisis: The Federal Reserve announced Wednesday that it would cut interest rates for the first time since the 2008 financial crisis in a bid to protect the U.S. economy from a global downturn.

In a statement following a two-day meeting in Washington, the central bank’s Federal Open Markets Committee (FOMC) announced it would cut its baseline interest rate range to 2-2.25 percent, a 0.25 percentage-point cut.

- The widely expected cut comes after Fed Chairman Jerome Powell and top bank officials suggested the bank would reduce borrowing costs as insurance against global headwinds and stagnant inflation.

- Cheaper money will be welcomed by President Trump, who has pressured the Fed into cutting rates for months. The president said Tuesday that he has been “very disappointed” in the Fed and wanted a “large cut.”

Even so, the Fed’s decision to cut rates reflects rising fears about threats to the record stretch of prosperity Trump inherited and is seeking to extend ahead of the 2020 election. I explain why here.

Why the Fed cut rates:

- For months, Powell and his colleagues have expressed concerns with lagging business investment and the potential harm from continued trade tensions, economic uncertainty and looming recessions in China and Europe.

- The U.S. economy still boasts a strong labor market, rising wages and booming consumer spending. But data released Friday by the Commerce Department showed growth slowing, hindered by a sharp downturn in business investment and other long-term indicators of economic success.

- The Fed has also sought to nudge inflation closer to its 2-percent annual target after a year of consistently running beneath that range.

“The performance of the economy has been reasonably good, the positioning of the economy is is as close to our objectives as it’s been in a long time, and the outlook is also good,” Powell told reporters Wednesday.{mosads}

“But again, the issue is more the downside risks and the shortfall and inflation and we’re trying to address those,” he added.

Why Wall Street freaked: Investors had expected Wednesday’s rate cut to be the first in a series intended to defend the U.S. economy from trade tensions and looming trouble in Europe and China. But Powell rejected that notion, explaining the Fed may not deem further cuts necessary.

Powell’s comments shook investors, who had bet on at least two to three more cuts before the end of the year, leading stocks to spiral down in the market’s worst day since May.

The Dow closed with a loss of 333 points, finishing 1.23 percent lower on the day. The S&P fell around 1.1 percent, while the Nasdaq fell 1.2 percent by Wednesday’s closing bell.

Why Trump got mad: It’s no secret that Trump reacts strongly to the performance of the stock market and frequently blasts the Fed for not doing enough to support it.

That’s part of the reason why Trump has been so insistent about pressuring the Fed into cutting rates. While Trump did get a rate cut Wednesday, it wasn’t the “large cut” he demanded–or the start of the string of cuts the stock market wanted.

“What the Market wanted to hear from Jay Powell and the Federal Reserve was that this was the beginning of a lengthy and aggressive rate-cutting cycle which would keep pace with China, The European Union and other countries around the world,” Trump tweeted.

“As usual, Powell let us down, but at least he is ending quantitative tightening, which shouldn’t have started in the first place – no inflation. We are winning anyway, but I am certainly not getting much help from the Federal Reserve!” he continued.

LEADING THE DAY

Senate kicks budget vote to Thursday amid questions over GOP support: The Senate has kicked the vote on a two-year budget and debt ceiling deal to Thursday amid lingering questions about whether a majority of Republicans will back the agreement.

GOP senators emerged from a closed-door lunch Wednesday saying they expected the budget vote would take place Thursday around noon.

Asked if senators would have the votes to pass the budget deal, Sen. John Thune (S.D.), the No. 2 Senate Republican, warned that “failure is not an option.”

“You’ve got a lot of members who are very eager to vote for it,” he added. “But you know all these votes, any spending vote or debt limit vote is never easy. … We’ve got members who obviously are probably not going to vote for it.” The Hill’s Jordain Carney tells us where things stand.

In a nutshell:

- There are lingering doubts about whether Republicans will be able to win a majority of their 53 senators to support the spending package, which cleared the House last week with only 65 GOP lawmakers voting for it.

- GOP leadership has been urging members to support the bill, arguing it provides a needed boost to defense spending and that the alternative was a debt default and deep spending cuts.

- But roughly a dozen GOP senators, including Sens. Mitt Romney (Utah), Marco Rubio (Fla.) and Rand Paul (Ky.), have said they would oppose the budget deal despite Trump’s blessing for the agreement. Several other Republican senators, including Sens. Thom Tillis (N.C.) and Tim Scott (S.C.), remain on the fence.

Judge leaning toward order that would keep Trump’s tax returns with NY: A federal judge in the District of Columbia said Wednesday that he’s leaning toward issuing an order under which New York wouldn’t provide President Trump’s state tax returns to House Democrats while the state argues certain motions.

“That is my current thinking,” Judge Carl Nichols, a Trump appointee, said during a teleconference with lawyers for New York officials, Trump and the House Ways and Means Committee — the parties in a lawsuit Trump filed last week.

Nichols said Wednesday that he is contemplating issuing an order that would allow the New York officials to argue that the federal court in D.C. doesn’t have jurisdiction over them and that the D.C. court is the wrong venue for the lawsuit.

The Hill’s Naomi Jagoda guides us through the legal battle here.

GOOD TO KNOW

- Senate Finance Committee Chairman Chuck Grassley (R-Iowa) said Wednesday that President Trump should tread lightly in his effort to persuade Speaker Nancy Pelosi (D-Calif.) to move forward with a revised version of the North American Free Trade Agreement (NAFTA).

- The Department of Housing and Urban Development (HUD) on Tuesday approved an agreement to settle allegations that a bank led by Treasury Secretary Steven Mnuchin and a top Trump-appointed bank regulator violated federal lending discrimination laws.

- The Federal Trade Commission (FTC) warned of fraudulent websites purporting to allow consumers to file a claim as part of Equifax’s $575 million settlement … but is also encouraging consumers to accept free credit monitoring since Equifax won’t have enough money to pay out all of the affected victims.

- House Ways and Means Committee Chairman Richard Neal (D-Mass.) on Wednesday warned the Trump administration against taking unilateral action to reduce capital gains taxes, as Republicans have stepped up their push for the administration to take such action.

ODDS AND ENDS

- The number of $100 bills in circulation surpassed the number of $1 bills for the first time, according to an International Monetary Fund report.

- Sens. Mike Crapo (R-Idaho) and Mark Warner (D-Va.) introduced legislation Tuesday intended to secure U.S. technological supply chains from exploitation from countries such as China.

- The $26 billion T-Mobile–Sprint deal faces one last major hurdle as a group of state attorneys general look to block the telecommunications mega-merger in court.