TCJA one year later: One broken promise after another

As we approach the one-year anniversary of the signing of the Tax Cut and Jobs Act (TCJA), Congress has some explaining to do.

The American people were made many promises if corporate tax rates were cut, many of which have been broken. The American people are getting massive deficits; deficits they, their children and grandchildren are responsible for. Promises made, promises broken, that’s the real TCJA one year later.

{mosads}TCJA proponents made five key promises in hawking the bill:

- massive wage growth;

- skyrocketing job growth;

- a tsunami of business investment;

- sustained 4-6-percent GDP growth; and

- no increase in deficits.

Broken promise No. 1: $4,000-$9,000 wage growth.

Americans were promised “an increase of $4,000 to $9,000 in wage and salary income,” if only the corporate tax rate was cut significantly. The story went that corporations would take their tax cut savings and shower their employees with generous raises.

While the corporate tax rate was cut significantly, wage growth has been less than promised. It’s been more of a trickle than a showering.

In the 11 months following the December 2017 signing of the TCJA, wage growth has grown $0.71 an hour. During the same 11 months in the year prior to the corporate tax cuts, wages grew at $0.59 an hour.

Assuming 2,000 hours of work in a year, that equates to a $1,420 increase to date, well-short of the $4,000-$9,000 promised.

Some may note that select companies gave highly publicized bonuses of $1,000. While better than nothing, it is important to remember that these were not wage increases. Rather, they were discretionary and, very likely, one-time events.

Broken promise No. 2: Nearly 1 million additional jobs.

Americans were also promised nearly 1 million jobs by House Speaker Paul Ryan (R-Wis.). Unfortunately for the American people, this too became just another broken promise.

In the 11 months following signing of the TCJA in December of 2017, the economy added 2.27 million jobs, according to Bureau of Economic Analysis data.

That sounds impressive until you realize that during the same 11 months prior to corporate tax cuts, the economy added 2.01 million jobs, resulting in only 255,000 more jobs being created after the TCJA was passed compared to the same period before it was passed. 255,000 jobs is only a little more than a quarter of what was promised, another broken promise.

Worse still, the nominal increase in job growth is already slowing to levels below those seen before passage of the TCJA. During the last three months, average job growth has sunk below 2017’s average job growth, not exactly the sustained job growth taxpayers were promised.

Not only did job growth fall well-short of what was promised, companies announced the firing of hundreds of thousands of Americans.

Verizon alone announced that it will be firing 44,000, while Kimberly-Clark added insult to injury, not only announcing the elimination of 5,500 jobs, but also that it would use savings from the TCJA tax cuts to fund the layoffs. So much for taking the tax cuts and increasing hiring.

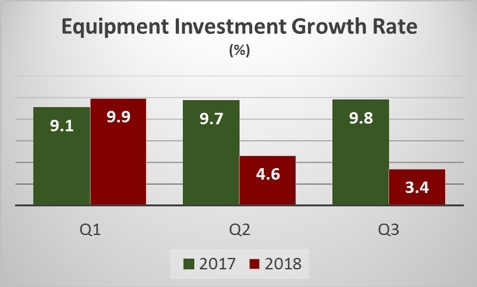

Promise No. 3: Sustained business investment tsunami.

Americans were also promised a tsunami of business investment with proclamations that tax cuts would spawn lasting increases in domestic business investment. Not only was the increase nominal, it was a very short-term increase with the rate of business investment growth now falling precipitously.

The average rate of growth in equipment investment in the first three quarters after passage of the TCJA has been less than the rate of growth experienced prior to passage of the TJCA: 6 percent vs 9.5 percent.

In fact, equipment investment grew nearly $30 billion less during the first three quarters after passage of the TCJA than during the same period the year before passage of the tax bill.

Source: Bureau of Economic Analysis

This investment figure is especially damning since the tax bill contained specific provisions promised to increase business investment, including immediate and 100-percent deductibility of equipment investment spending.

Where did the corporate tax cut saving go? Companies have been shoveling their mountainous tax savings into dividends and share buybacks. Goldman Sachs estimated that companies will spend $1 trillion on share repurchases in 2018. That would be nearly 50-percent more than in 2017. Mystery solved.

Broken promise No. 4: Sustained 4-6-percent GDP growth

Americans were confidently promised increasing and sustained GDP growth, 4-6 percent to be exact. Instead, GDP growth reached 4.2 percent for a single quarter and is now declining.

Having looked at the steady decline in equipment investment and skyrocketing increase in share buybacks this should not be surprising. While share buybacks help stockholders, unlike business investment, they don’t directly increase GDP.

Broken promise No. 5: No increase in deficits

Proponents of the TCJA also promised that there would be no increase in deficits. While that would have been nice, that certainly hasn’t been the case. Not only has there been a massive increase, it is worse than originally estimated.

According the Congressional Budget Office’s April update, the TCJA will increase the federal debt by nearly $1.9 trillion over the next 10 years. Not only is that a staggering number, it is $433 billion more than the December estimate provided by the Joint Committee on Taxation.

The 2018 federal deficit was $779 billion, up more than $100 billion from the 2017 deficit of $666 billion. Not coincidentally, 2018’s corporate tax revenue was nearly $100 billion less than 2017’s level, and it is expected to get much worse. The White House estimates that the 2019 deficit will reach $1.1 trillion.

Fixing the fatal flaw of the TCJA

All of the broken promises were created by one fatal flaw in the TCJA: unconditionality. The corporate tax cuts in the TCJA were unconditional. Company tax rates were reduced independent of whether they actually raised wages or hired more Americans.

{mossecondads}Companies firing Americans received the same tax cuts as companies hiring Americans. There is a simple solution: Tie each company’s tax rate to its rate of wage and job growth. Increase employee pay or hire more Americans, and you’ll pay a lower tax rate. It’s not rocket science.

While some politicians proclaim the importance of incentives, when it came to the TCJA, they mysteriously absolved corporations of any responsibility for earning tax cuts.

Instead, the TCJA’s unconditional tax cuts created perverse incentives for companies to use their tax cuts savings to fire Americans. One year later, Congress has some explaining to do for the TCJA’s many broken promises.

Chris Macke is the founder of Solutionomics, an online platform focused on developing solutions for a more efficient, merit-based corporate tax code. He provides market updates and implications of monetary policy changes to the Federal Reserve and is a contributor to the Fed Beige Book. Find him on Twitter @solutionomics.

Copyright 2023 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed. Regular the hill posts

The Hill Podcasts