President Trump vowed to never again sign a bill like the massive omnibus that was released at the last minute and set spending levels for a year that was already half over.

There was good reason to dislike it — not only is procrastination a terrible way to govern, the bill also spent more money than either side even asked for, busting through budget caps and adding $320 billion to deficits.

Bipartisan agreement came only when each side let the other go on a spending spree with the national credit card.

{mosads}In response to backlash from fiscal hawks, the administration has dusted off a process known as rescission, which allows the president to clawback some funds through a streamlined process.

At one point, there were rumors of as much as $60 billion in rescissions. In the end, the White House proposed a much smaller $15 billion package that scraped through the House on a vote of 210 to 206 and failed Wednesday in the Senate 48-50.

Because many of the funds from the proposal were not going to be spent anyway, the Congressional Budget Office says the bill would have reduced deficits by little more than $1 billion over 10 years — or .002 percent of federal spending during that time frame.

It is the federal budget equivalent of loose change between the sofa cushions.

There really couldn’t be any lower fiscal fruit to pick than reclaiming fractional amounts of unspent money, but Congress is having a difficult time even agreeing to that.

The fight over rescissions is a much bigger deal than people realize. It illustrates plainly that Congress struggles mightily to make even the smallest responsible fiscal decisions at a time when gigantic decisions are just around the corner.

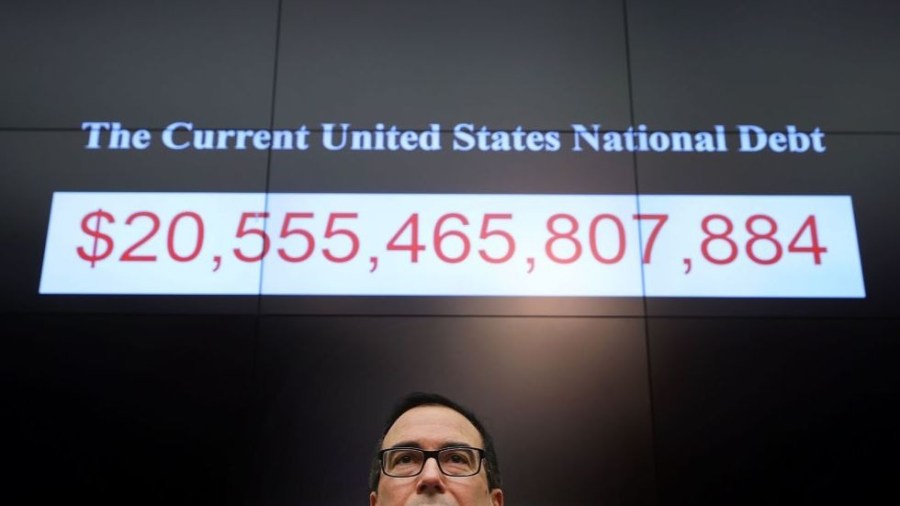

The trustees of Social Security recently released their annual report reminding us of the looming shortfall in the program’s funding. It is one of five major national trust funds going insolvent during the next 16 years — a funding crisis totaling in the trillions.

This comes at a time when our national debt as a share of the economy is already surging toward record highs not seen since World War II. In two years, trillion-dollar annual deficits return forever.

In just over a decade, trillion-dollar annual interest payments will gobble up a larger share of the federal budget. By 2023, the nation will be spending more on interest payments each year than it does on Medicare or defense.

It’s hard to believe that at the turn of the century, we were running annual budget surpluses and worried about what would happen if we paid off the national debt.

Then in the span of only 20 years, because of deficit-financed legislation and unforeseen events ranging from wars to terrorism to recession to natural disasters, our debt is now headed to never-before-seen highs.

The continued denial of what’s coming has gone from frustrating to frightening. A plan to make our trust funds solvent and put the debt on a sustainable, downward path as a share of the economy will require tough decisions and a real national moment of bipartisanship and shared sacrifice. There is no magic solution to the problem.

While the debt-financed tax cuts added some stimulus to the economy (at a time we didn’t need it) this will prove to be a sugar high and the additional debt will likely outweigh the gains. The drag of the debt and aging of the population mean that growth will fall back to a long-term rate around 2 percent in a few years.

Policymakers should strive to pass pro-growth policies, but they should not count on growth to sidestep needed choices to cut spending and raise revenue.

While many in Washington see rescission as an election year stunt, it might be wiser to look at the bigger picture. If Congress can’t agree to save $1 billion in unspent money over a decade, we are in big, big trouble. Because that is one of the easiest fiscal decisions we will face for quite a while.

Maya MacGuineas is the president of the Committee for a Responsible Federal Budget and head of the Campaign to Fix the Debt.