Hemorrhaging losses, the Fed’s problems are now the taxpayer’s

When liabilities exceed assets, equity capital is negative and an entity is technically insolvent. Few institutions in that condition can continue operating at a loss indefinitely, and those that can usually benefit from an explicit government guarantee. Past special cases have included government-backed agencies like the U.S. housing GSEs.

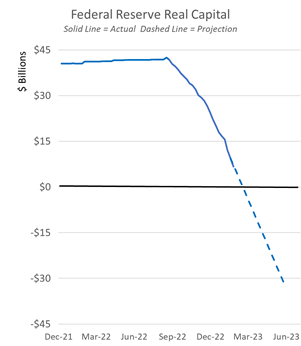

From mid-March 2023, there will be a new addition to the list of institutions that, while losing billions of dollars a month and technically insolvent, with the benefit of taxpayer support will still be able to issue billions in new interest-bearing liabilities. That institution is the Federal Reserve.

With large projected operating losses and liabilities already in excess of assets, existing creditors are unlikely to be repaid, let alone new creditors. No sensible fiduciary would lend under these conditions unless newly injected funds have seniority in bankruptcy or carry an explicit government guarantee.

Since mid-September, the Federal Reserve has lost about $36 billion and will continue to post billions of dollars a month in losses for many months if not years to come. Fed losses have already consumed about 85 percent of its stated capital of $42 billion. It will take less than 3 weeks for the Fed to burn through the $6.6 billion of its remaining capital.

The Fed routinely creates new money by purchasing interest-bearing U.S. Treasury securities in exchange for newly created Federal Reserve notes or interest-bearing bank reserves. From mid-March on, the Fed will, for the first time in its history, pay for its accumulating losses by issuing new liabilities without acquiring any new interest-bearing assets. The Fed will pay its bills by printing new money — not just Federal Reserve Notes that pay no interest, but by issuing new reserve balances that pay banks an interest rate higher than can be earned in a savings account.

When the housing GSEs were insolvent and losing money hand-over-fist, the U.S. Treasury used congressional powers in the Housing and Economic Recovery Act of 2008 to inject enough new capital to save the GSEs from defaulting so they could continue to borrow and operate. How can a technically insolvent and loss-hemorrhaging Federal Reserve continue to operate without a similar congressionally-approved bail-out? Do other central banks have the Fed’s seemingly magical power to continue operations while technically insolvent, and yet still issue billions in new interest-bearing liabilities to cover losses?

The “magic” begins with the fact that, regardless of the size of its accumulated losses, the Fed will always report positive equity capital. By any sensible accounting standard, losses reduce retained earnings and capital. Nothing is more basic. The Fed’s real capital is its stated capital of $42 billion minus its accumulated losses. The Fed magically suspends this law of accounting by booking its accumulated losses as an asset. If Fed losses accumulate to $100 billion, as they probably will in 2023, or to $200 billion or more by 2024, the Fed will report that it still has $42 billion in equity capital. Magic.

The Fed and many economists believe that the Fed’s losses and its looming negative capital position are inconsequential. While other central banks shrug-off losses, they are not so cavalier with their accounting treatment of losses, nor do they contend that their capital position is of no consequence.

In reporting its recent losses, the European Central Bank canceled paying dividends and was careful to state that its losses were well covered by its reserves and so had no impact on its capital. The Swiss National Bank’s $143 billion loss in 2022 caused it to cancel its dividend payments and reduce its retained earnings. It still remains well-capitalized by central bank standards. In Great Britain, His Majesty’s Treasury explicitly agreed to offset losses of the Bank of England, and the Canadian Finance Ministry has a contract with the Bank of Canada to offset any realized losses on its QE bonds. Meanwhile, the Dutch central bank alerted its country’s Treasury of the possibility that the bank might need to be recapitalized. For all of these central banks, their equity capital position apparently does matter.

With negative real capital and massive losses accruing, how will the Fed still pay member banks a dividend, interest on their reserves balances, conduct monetary policy and pay its bills? With the benefit of an implicit government guarantee — a guarantee that has so far avoided any mention in congressional hearings.

On a consolidated government basis, the Fed’s accounting treatment — paying for accumulating losses by creating new interest-bearing liabilities — is equivalent to the U.S. Treasury selling new interest-bearing debt and remitting the proceeds to the Fed to cover its losses. If Fed losses were paid and accounted for in this way, the Fed’s losses would count against the Federal budget deficit and the new Treasury debt issued would add to the Federal government’s outstanding debt.

With the Fed counting its accumulating losses as a deferred asset, the losses do not reduce the Fed’s reported equity capital or increase the federal budget deficit. Moreover, the new interest-bearing liabilities the Fed issues to pay bank dividends, interest on bank reserves and to cover other Fed operating costs do not count as part of the U.S. Treasury’s outstanding debt.

The Fed’s accounting trickery allows the Fed to borrow taxpayer money to cover its losses without the borrowing or the losses appearing on the Federal government’s ledgers. The Fed itself decides how much to borrow from taxpayers without any explicit congressional authorization. The current arrangement inadvertently allows the Fed to appropriate, borrow and spend taxpayer dollars on its own authority — an issue that should be addressed in the Fed’s next semi-annual congressional appearance.

Paul H. Kupiec is a senior fellow at the American Enterprise Institute. Alex J. Pollock is a senior fellow at the Mises Institute and the co-author of the new book, “Surprised Again!—The Covid Crisis and the New Market Bubble.”

Copyright 2023 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed. Regular the hill posts

The Hill Podcasts