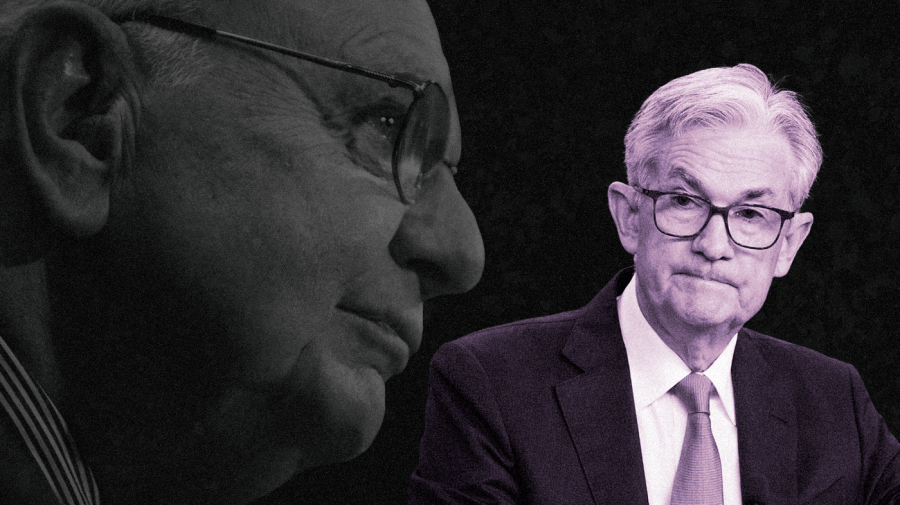

The ghost of the early 1980s recession is haunting the Federal Reserve.

With inflation still near 40-year highs and the U.S. economy slowing, the Fed’s aggressive rate hikes have fueled concerns of a central bank-induced recession akin to the one triggered by former Fed Chairman Paul Volcker during the 1980s. While Volcker’s rate shock ended two decades of rising inflation, it did so at the cost of a severe recession.

Fed Chairman Jerome Powell has frequently praised Volcker’s refusal to back down and channeled that persistence into his own battle with inflation. But most economists believe Powell can wage a far less costly war against rising prices, given major shifts in the economy — and Fed policy — since the days of Volcker.

“Inflation looks like it has already peaked and never got near the 14.5 percent peak reached in 1980, so the Fed will not have to raise rates as high as it did back then,” said Eric Swanson, an economics professor at the University of California, Irvine.

“We also benefit today from the experience that we gained back then: Everyone knows that inflation was high and was successfully brought down with high interest rates, so we know the Fed can do it again,” he said.

‘The Fed made a big mistake’

The Fed has spent much of the past year attempting to course-correct from its earlier misjudgments of how high inflation would climb.

Fed officials resisted raising interest rates from near-zero levels for much of 2021, even as prices began rising at faster rates. Powell and key Fed leaders expressed confidence that high inflation would come back down toward the bank’s 2 percent annual target once the U.S. quashed COVID-19 for good and the world economy recovered from a serious shock.

But inflation surged deeper into the year as a series of pandemic-related supply chain snarls, COVID-19 outbreaks and a persistent labor shortage drove prices higher than Fed officials expected. Powell acknowledged in December 2021 that the Fed should have begun raising rates sooner, laying the groundwork for a record-breaking span of rate hikes in 2022.

“I think [Volcker] would agree that the Fed made a big mistake by not starting to raise interest rates sooner in late 2021 and early 2022, but that the overall pace of rate increases in 2022 was appropriate and that the Fed’s current plan to bring inflation down is the right one,” Swanson said.

The Fed has raised interest rates a whopping 4.5 percentage points since March 2021 through eight rate hikes in as many meetings. The bank issued four straight increases of 0.75 percentage points beginning in June — when annual inflation peaked at 9.1 percent, according to the Labor Department’s consumer price index — boosting borrowing costs at a historically quick pace.

Inflation has since fallen to an annual rate of 6.5 percent as of December. The Fed’s preferred inflation gauge, the personal consumption expenditures price index, dropped to an annual increase of 5 percent after peaking at 7 percent in June.

Milton Ezrati, chief economist at Vested, said the Fed’s swift pivot and aggressive rate hikes mark a key difference between the Powell era and the surge of inflation that preceded Volcker.

“In the 1980s, inflation and inflation expectations had over 10 years to build and embed themselves into economic thinking at every level,” Ezrati said.

The Fed waffled on tackling inflation throughout much of the 1960s and ‘70s, holding off on rate hikes under immense political pressure from presidents unwilling to allow higher unemployment on their watch. The bank’s refusal to act prompted workers to keep asking for ever higher wages, which pushed businesses to keep raising prices to compensate.

The unemployment rate soared to a peak of 10.8 percent in November 1982 after three years of excruciating rate hikes under Volcker. The Fed’s baseline interest rate peaked at nearly 22 percent, more than five times higher than the bank’s current level. And the recession was particularly devastating for the U.S. manufacturing sector and communities that depended heavily on goods production.

“If the Fed continues as it finally set out to do last March, the economy can avoid the pressure that had built back then and so resolve the matter faster than in the 1980s.”

‘Very difficult to manage the risk’

The ‘80s wage-price spiral and the recession left in its wake scarred generations of policymakers, including Powell, who has effusively praised Volcker’s willingness to defeat inflation at any cost.

Without quashing inflation now, Powell argued Wednesday, price growth could run beyond the Fed’s control and only come down with a crushing recession.

“It’s very difficult to manage the risk of doing too little and finding out in six or 12 months that we actually were close but didn’t get the job done, inflation springs back and we have to go back in,” Powell said Wednesday after the Fed boosted rates by 0.25 percentage points and hinted toward more to come this year.

“We have no incentive and no desire to overtighten,” Powell said, referring to risk of the Fed raising rate high enough to cause a recession.

“But … if we feel like we’ve gone too far and inflation is coming down faster than we expect, then we have tools that would work on that,” he continued.

As inflation falls and the job market holds strong, most economists are confident the Fed won’t need to derail the economy for years to bring prices down. The unemployment rate dropped to 3.4 percent in January, according to the Labor Department’s monthly jobs report, all while wage growth continued to drop and relieve some pressure on inflation.

The steady decline of inflation from June’s peak may prove that the U.S. can avoid a debilitating recession driven by double-digit Fed interest rates.

“Last year, some senior economists like Larry Summers were saying that these drastic measures were necessary,” said Dan Altman, chief economist at gig economy site Instawork.

“But now, we’ve had inflation declining without a corresponding increase in unemployment. The economy may not have to go into recession to bring inflation under control,” he added.

Some experts, however, fear the Powell Fed may be driving the U.S. into a needless recession with more rate hikes, even if it won’t be as bad as the one induced by Volcker. Fed rate hikes are notoriously slow to trickle through the economy, and even bank officials acknowledge that the full slowing impact of higher borrowing costs has not yet been felt.

If the Fed has already boosted rates enough to slow the economy toward its 2 percent annual inflation target but keeps increasing them anyway, the steady job market could falter and throw the economy into a downturn.

“Don’t be fooled by Powell’s words of optimism about bringing down inflation without damage to the labor market,” wrote Skanda Amarnath, executive director of research group Employ America, in a Wednesday analysis.

“Even if the unemployment rate starts ticking up and recession risks snowball, the Fed’s current stance is that they will stay idle and only consider easing after it is too late. Not great,” he added.