Warning to US banks: Chinese risks are closer than they appear

Moody’s recent downgrade of China and Hong Kong should signal to bank risk managers and bank regulators that they need to verify that large banks can calculate their credit and market risk exposures to East Asia. Moody’s downgraded China from A1 to Aa3 on May 24. The rating agency had last downgraded China 23 years ago, in June 1989 during the Tiananmen Square Massacre.

Moody’s analysts downgraded China last week because, “China’s financial strength will erode somewhat over the coming years, with economy-wide debt continuing to rise as potential growth slows.” Chinese indebtedness is fast approaching 300 percent of GDP. Within a day, Moody’s also downgraded Hong Kong to Aa2 from Aa1.

{mosads}Moody’s view is that “Credit trends in China will continue to have a significant impact on Hong Kong’s credit profile due to close and tightening economic, financial and political linkages with the mainland.”

According to data in the Federal Financial Institutions Examination Council’s E16 Country Exposure Lending Survey and Country Exposure Information Report, U.S. banks’ credit exposure to China has reached $83 billion. That exposure represents less than 0.5 percent of U.S. banks’ total domestic and foreign exposures.

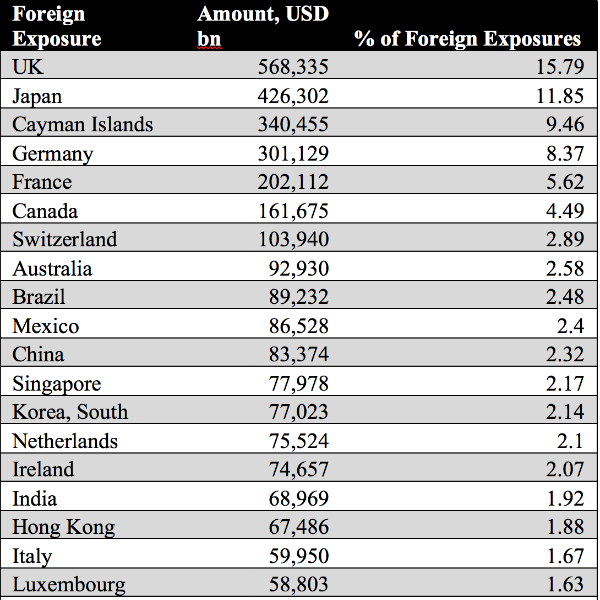

When we look only at U.S. banks’ foreign exposures, China ranks 11th, representing 2 percent of all foreign exposures. To put this into context, U.S. banks’ largest foreign exposures are to the U.K.($568 billion) and Japan ($426 billion), representing 16 percent and 12 percent, respectively, of total U.S. banks’ foreign exposures.

While U.S. banks’ credit exposure to China is small on a relative basis, it is important to note that in just one decade, that exposure has grown about 225 percent from $26 billion at the end of 2007. Banks in the U.S. now have the second-largest exposure to China, after the U.K., which has exposures of roughly $155 billion, according to the Bank for International Settlements.

Source: FFIEC E16 Country Exposure Lending Survey and Country Exposure Information Report

Banks in the U.S. have limited credit exposure in Hong Kong at only $67 billion. What should give us pause is that when you add up the exposures of the very interconnected China and Hong Kong financial systems, U.S. banks’ exposure is almost $151 billion, or a few billion dollars higher than U.S. banks’ total exposure to Switzerland.

American banks are exposed to China and Hong Kong directly because they buy Chinese and Hong Kong debt and have financial transactions with Chinese and Hong Kong financial institutions and corporations.

It is also incredibly important to remember that not only are U.S. banks directly exposed to China, but so are myriads of other types of U.S. financial institutions and corporations. In turn, U.S. banks are exposed to those financial institutions and corporations because the banks lend to them, invest in their bonds and equities and, in some cases, invest in them directly. If Chinese economic conditions continue to worsen, U.S. companies and banks would also get hurt from stock and bond market turmoil in Asian financial markets.

Moreover, the largest U.S. financial institutions, especially large banks, often transact credit derivatives linked to Chinese and Hong Kong sovereign, corporate and financial institution debt, as well as the debt of other global companies impacted by Chinese developments. The extent of those contingent liabilities is difficult to measure since parties transacting credit derivatives do not have to report publicly on what type of debt they are paying protection.

What is usually not discussed at all is that the U.S. banks’ two largest exposures are to the U.K. and Japan, for which China represents very large foreign exposures. Hence, any negative repercussions that would impact U.K. and Japanese financial institutions and corporations from a Chinese slowdown would end up trickling down to U.S. banks, even if with a lag.

Moreover, in the U.S. banks’ top-20 foreign exposures, they also have Australia, South Korea, Singapore and Taiwan, all of which hold China as an incredibly significant counterparty.

Already, the Taiwanese bank regulator has asked its banks to diversify away from mainland China. It is not unreasonable that U.S. bank regulators should, at the very least, ask the largest banks in the U.S. to calculate their exposure to China and to those countries that could be most negatively affected by the economic slowdown and high leverage of the Chinese economy.

JPMorgan Chase, Wells Fargo, Bank of America and Citibank have the largest exposures to China. They should demonstrate that they have high quality and complete data sets to calculate their primary and secondary credit exposures there. The Basel Committee on Banking Supervision released “Principles for Effective Risk Data Aggregation and Risk Reporting” in 2013 and recommended that banks comply with these principles by 2016.

These principles ask banks to improve their data collection and to invest in better systems so that they can improve their credit, market and operational risk measurements. Banks regulators are well within their right to apply these principles to big banks’ ability to measure theses risk exposures to China.

If these big banks cannot calculate accurately and quickly their exposures to China presently, banks’ risk managers and bank regulators should doubt that these banks could calculate those exposures in a period of market stress.

Mayra Rodríguez Valladares is managing principal of New York-based MRV Associates. Previously, she was at the Federal Reserve Bank of New York and JPMorgan Chase. Follow her on Twitter @MRVAssociates.

The views expressed by contributors are their own and not the views of The Hill.

Copyright 2023 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed. Regular the hill posts

The Hill Podcasts